Cash Buyers - Decreasing In The Las Vegas Market

That means more opportunities for buyers who are financing. Many sellers were choosing cash buyers over borrowers.

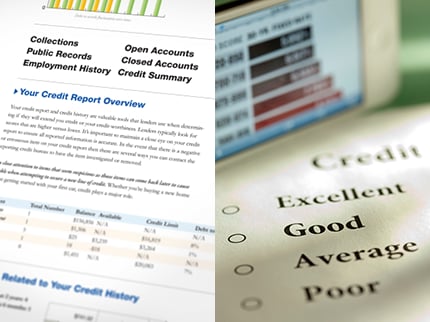

If you are thinking about purchasing a home, your credit is important. Here are some steps to take to make sure that you are creditworthy to purchase your dream home.

First, find out what your credit report says. You can review your credit report for free at AnnualCreditReport.com.

When you retrieve your free report, look for errors when reviewing your credit report.

- Review your pay history for all current and paid-in-full accounts.

- Check your payment timelines for errors or late payments.

- Check any collection or charge-off accounts that are reported as outstanding when you know they have been paid.

If you find errors, you can contact the credit bureaus directly via Phone:

- Experian: (888) 397-3742

- Equifax: (800) 846-5279

- Trans-Union: (800) 916-8800 Option 3

Online:

- You can initiate a dispute online. When using this option, Equifax and Experian will provide updates to your request via mail.

Written Request:

- Experian must be done online or via phone

- Equifax: P.O. Box 740241, Atlanta, GA 30374

- TransUnion: P.O. Box 403, Springfield, PA 19064

Sample dispute letters can be found on the FTC website.

Next find out what your credit score is. Visit MyFICO for your current FICO scores from TransUnion and Equifax. You can also go directly to each one of the credit bureaus to get your score. Experian is the third credit reporting bureau that you should visit.

Next find out what your credit score is. Visit MyFICO for your current FICO scores from TransUnion and Equifax. You can also go directly to each one of the credit bureaus to get your score. Experian is the third credit reporting bureau that you should visit.

Your FICO score information is weighted and divided based on the following percentages:

35% Payment History

-

The number of accounts that are past due or delinquent compared to the number of accounts that are in good standing.

-

The first delinquent item will have the most negative impact. Example: A person who has a 700+ score reports a 30-day late payment on his mortgage. This can have a much larger impact than a borrower who has a score in the low 600s who reports a 30-day late payment and has other late credit card payments.

-

A lengthy credit history will generally increase your score. Nonetheless, if you manage credit responsibly, you can get a high credit score with a short credit history.

-

Public record items negatively impact your score.

-

Civil judgments

-

Federal tax liens

-

State tax liens

-

Bankruptcy filings

30% Amount Owed On Revolving Accounts

-

Balances on revolving debt should remain below 30% of the credit limit.

-

Chase, CITI, and Macy's do not report the credit limit. At this time, there is no resolution.

-

HELOCs can be considered revolving credit. If the account was closed, it appears as $0, causing the account to appear to be over the credit limit.

-

Student loans, such as a Parent Plus Loan, incur interest while in deferment. The loan balance appears higher than the original amount, which can result in a negative impact on your FICO score.

-

The number of accounts reporting a balance can indicate that the person is overextended.

15% Credit History

-

FICO will not generate a score if the creditor's file has been dormant for over 6 months.

-

If a person becomes an authorized user on an existing account, that may add credit history to a thin credit file, which may boost the FICO score. If you are applying for a mortgage, check with your loan officer to find out if this will help.

10% New Credit Accounts

FICO scans the credit file and searches for open dates within the last 24 months. FICO compares these to the established accounts.

Don't open new credit accounts prior to applying for a home mortgage.

What Happens If You Have Bankruptcy?

-

The first 24 months have the most impact.

-

The impact depends on your history.

-

The statute of limitations on a Chapter 7 is 10 years from your discharge date.

-

Statute of limitations on a Chapter 13 is 7 years from your filing date.

-

Rebuild your credit as soon as possible:

-

Get a secured card from a local bank or credit union

-

Maintain a balance lower than 30% of the available credit

-

Make all payments on time

-

Within 6 months, your credit history will be included in your score.

How long before you can apply for a mortgage?

Conventional Loan

-

Chapter 7 is 4 years from the discharge date.

-

Chapter 13 is 2 years from the discharge date or 4 years from the dismissal date.

-

Multiple bankruptcy filings are 5 years if more than one filing within the past 7 years.

FHA Loan

-

Chapter 7 is 2 years from the discharge date.

-

Chapter 13 is 1 year from the end of the repayment plan. Pay history must be good. A creditor must have permission from the court.

VA Loan

- Chapter 7 is 3 years from the discharge date.

-

Chapter 13 is 1 year from the end of the repayment plan. Pay history must be good. A creditor must have permission from the court.

USDA Loan

-

Chapter 7 is 3 years from the discharge date.

-

Chapter 13 is 3 years from the discharge date.

Notes

-

Your lender will ask for an explanation letter for all inquiries reporting on your credit report for the previous 120 days.

-

Many people are not aware that when you apply for a loan, the scores that the lenders use may be different than what you retrieve. The lenders use a different algorithm so there may be a slight difference.

-

Co-signers are considered fully responsible for the entire amount of the loan.

-

To Calculate your mortgage, check My Mortgage Calculator